![]()

Kalam IAS Academy was founded by a team of committed individuals who believe that the traditional way of UPSC preparation needs to be changed.

IE Explained: RBI unlocks capital market liquidity with funding boost at a time markets are flat: Here’s how the measures would work

Syllabus: Pre/Mains – Economy

Why in News?

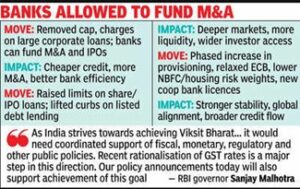

RBI launched major regulatory reforms (22 key measures) to ease capital access and revitalize bank-market lending amid weak equity flows.

IPO Financing Relaxation

- Limit ↑ → Retail IPO funding cap raised from ₹10 lakh → ₹25 lakh per person.

- Market context → Megacorps like Tata Capital, LG India IPOs expected soon; strong pipeline of billion-plus issues.

- Bank/NBFC exposure → As of July 2025, banks’ advances against shares & bonds = ~₹9,730 crore; NBFCs’ ~₹22,432 crore (Dec 2024)

- Impact → More retail/institutional subscriptions; deeper primary market; channel savings into equity markets.

- Risk → Overextension on IPOs in frothy valuations; need credit assessment for funded investors.

Lending Against Securities

- Share-backed loan limit jump → From ₹20 lakh → ₹1 crore per individual (5× increase).

- Ceiling on listed debt removed → Regulatory cap on lending vs listed debt (e.g. corporate bonds, debentures) abolished.

- REITs / InvIT units → Lending limits for these instruments raised under revised capital market exposure norms.

- Usage case & commentary → Zerodha’s Nithin Kamath welcomed the higher LAS (loan-against-securities) cap, citing that many retail investors still resort to high-interest personal/credit card debt despite holding stocks.

- Benefits → Investors can get liquidity without selling their holdings; banks/NBFCs can expand capital-market-backed lending books.

- Risk → In volatile markets, pledged shares may fall; margin calls, forced selling risk; overleveraging dangers.

Large Borrowers Rule Scrapped

- 2016 curbs withdrawn → The “Guidelines on Enhancing Credit Supply for Large Borrowers” (targeting groups with ≥ ₹10,000 crore exposure) will be shelved.

- Replacement → Large Exposure Framework (LEF) already caps exposure per bank to a borrower/group — system-level concentration will be managed via macroprudential tools.

- Impact → Corporates gain easier access to bank credit; banks have more flexibility in funding large projects, M&A, expansions.

NBFC Funding for Infrastructure

- Risk weights reduced → Loans by NBFCs to operational, high-quality infrastructure projects will carry lower risk weights.

- Rationale → Operational projects are less risky than construction stage; capital requirement relief enables NBFCs to lend more.

- Sector response → Infrastructure financing stocks (HUDCO, IREDA, PFC) jumped over 5% after the announcement.

- Benefit → Cheaper credit for roads, renewables, urban transport; fill infrastructure funding gaps.

- Risk → NBFCs over-expose to limited infra assets; credit concentration, default risk if project cashflows stress.

ECB Relaxation (External Commercial Borrowings)

- Borrowing flexibility → Proposed cap change: firms can borrow up to US$1 billion or 300% of net worth (whichever is higher).

- Cost caps scrapped → Remove rigid interest rate ceilings; allow market‐based rates (except short term).

- Expanded eligibility → More borrowers/lenders; relaxed end‐use restrictions; simplified reporting.

- Impact → Easier overseas credit sourcing for firms; lower funding cost; more capital inflow.

IFSC Forex Account Flexibility

- Repatriation window extended → From 1 month → 3 months for foreign currency accounts in IFSC (e.g. GIFT City).

- Parity with offshore → Aligns onshore IFSC accounts with offshore norms; better exporter flexibility.

- Effect → Greater forex liquidity in IFSCs; attract exporters to route via GIFT City/IFSC banking units.

Context & Significance

- FPI outflows → $2.7 billion withdrawn in September alone; Jan–Sep 2025 outflows = $17.6 billion (second highest in 9-month span).

- Equity market drag → In past year, Nifty fell ~4%, lagging regional peers; sentiment weak.

- Economic targets → RBI revised FY26 GDP outlook to 6.8% (↑ from earlier 6.5%) while lowering inflation forecast to 2.6%.

- Banking growth → Credit growth was ~10% YoY as of early September—below desired levels.

- Balancing act → Growth push via credit & liquidity; safeguards via macroprudential oversight.

Test Your Knowledge 01

Q. With reference to Loans Against Securities (LAS), consider the following:

- They are treated as unsecured loans by banks.

- They are considered a form of retail credit exposure.

- Over-leverage through LAS may exacerbate stock market volatility during downturns.

Which of the above is/are correct?

(a) 1 & 2 only

(b) 2 & 3 only

(c) 1 & 3 only

(d) 3 only

Hint:

- LAS are secured (backed by shares/bonds), not unsecured → eliminate 1.

- Retail product offered by banks/NBFCs → 2 is correct.

- Pledging + market fall = forced selling risk → 3 is correct.

Q. Foreign Portfolio Investors (FPIs) withdrawing $21 billion from Indian equities in 2024–25 has the following implications:

- Downward pressure on rupee

- Reduced equity market liquidity

- Lower current account deficit

- Greater role for domestic institutions in market stability

Select the correct answer:

(a) 1, 2 & 3 only

(b) 1, 2 & 4 only

(c) 2, 3 & 4 only

(d) 1, 2, 3 & 4

Hint:

- FPI selloff = ₹ pressure (1 ✔).

- Outflows = ↓ liquidity in equities (2 ✔).

- CAD impact? Outflow is capital account, not current → 3 ✘.

- Domestic institutions (mutual funds, LIC, etc.) step in → 4 ✔.

Q. Consider the following pairs (Reform : Likely Impact):

- IPO financing limit ↑ : ↑ Retail market participation

- Loans Against Securities (LAS) limit ↑ : ↑ Liquidity for HNIs

- xternal Commercial Borrowing (ECB) relaxation : ↓ Domestic savings rate

- NBFC infra risk weight ↓ : ↓ Cost of infra credit

Which of the above pairs are correctly matched?

(a) 1, 2 & 4 only

(b) 1, 2 & 3 only

(c) 2, 3 & 4 only

(d) 1, 2, 3 & 4

Hint:

- IPO financing ↑ = More retail access (1 ✔).

- LAS ↑ = More liquidity to HNIs (2 ✔).

- ECB relaxation = cheaper foreign funds, not ↓ domestic savings (3 ✘).

- Lower NBFC infra risk weight = cheaper infra lending (4 ✔).

IE Explained: Rise in cybercrime, most crimes against women in UP: How to read NCRB’s 2023 Crime in India report

Syllabus: Pre/Mains – Society

Why in News?

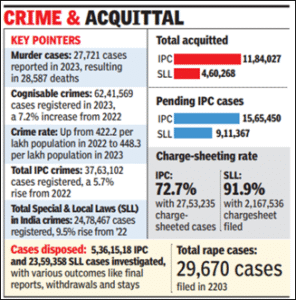

NCRB released Crime in India 2023 report → ↑ cybercrime, crimes against women & SC/STs

NCRB & Data Collection

- Est. 1986 → under MHA, compiles national crime data

- Sources → States/UTs police stations → validated district/state → NCRB software

- Method → Crime per lakh (population est. from 2011 Census projections)

- Limitation → Principal Offence Rule (only most serious crime counted) → underreporting

- Records only registered crimes → may reflect ↑ reporting, not always ↑ incidence

Key Findings 2023

Overall Crime

- Total crime rate ↑ 422.2 (2022) → 448.3 (2023)

- Murder ↓ 2.8% → 27,721 cases

- Crimes affecting human body ↑ 2.3% → 11.85 lakh cases

- MV Act violations doubled → 94,450 → 1.92 lakh

Crimes Against Women

- Total → 4,48,211 cases (↑0.7%) | Crime rate: 66.2/lakh female pop

- Top state: UP (66,381) > Maharashtra, Rajasthan, WB, MP

- Major categories → Cruelty by husband/relatives (29.8%), Kidnapping (19.8%), Outraging modesty (18.7%), POCSO (14.8%)

- Decline: MP, Maharashtra; ↑: Bihar, TN; Delhi UT highest (2,278)

Crimes Against Children

- 1,77,335 cases (↑9.2%)

- Kidnapping/abduction → 79,884 (45%)

- POCSO Act → 67,694 (38.2%)

Crimes Against SC/ST

- SCs → 57,789 cases | UP highest (15,130) > Rajasthan (8,449) > MP (8,232) > Bihar (7,064)

- STs → 12,960 cases (↑28.8%) | Manipur worst-hit, then MP (2,858), Rajasthan (2,453)

Cybercrime

- ↑31.2% → 86,420 cases | Rate 6.2/lakh pop

- Motives → Fraud (68.9%, 59,526 cases), Extortion, Sexual exploitation

- States: Karnataka, Telangana, UP top contributors

- Trend steady ↑ → 27,248 (2018) → 65,893 (2022) → 86,420 (2023)

How to Read the Report

- Data ≠ actual crime incidence → reflects registered crime

- ↑ numbers may indicate better reporting, e-FIRs, women helpdesks

- Principal Offence Rule → masks secondary crimes (e.g. murder+rape → only murder)

- Population base outdated (2011 census) → distortion in crime rate comparison

Test Your Knowledge 02

Q.Which of the following best explains the Principal Offence Rule used by NCRB in compiling crime statistics?

(a) A case is counted under all the sections of IPC applied to it.

(b) Only the first registered offence is counted for statistical purposes.

(c) Only the most serious offence in a case is recorded for the report.

(d) All crimes against women and children are recorded separately from other offences.

Hint: “Murder with rape” counted as only Murder.

Q. Consider the following with respect to Cybercrime in India (2023):

- It showed a steady rise since 2018.

- Fraud accounted for nearly 70% of cases.

- Maharashtra reported the maximum number of cases.

- The cybercrime rate per lakh population was higher than that of crimes against women.

How many of the above statements are correct?

(a) Only one

(b) Only two

(c) Only three

(d) All four

Hint: Trend ↑ since 2018 ✔, Fraud ~69% ✔, Top states = Karnataka/Telangana/UP ✘ (not Maharashtra), Cybercrime rate (6.2) << Women crime rate (66.2) ✘.

Nations must prepare to deal with stablecoins: FM Nirmala Sitharaman

Why in News?

FM Nirmala Sitharaman: Nations must prepare to deal with stablecoins → crypto innovations reshaping money & capital flows.

Stablecoins & Monetary Architecture

- Defn → Crypto pegged to assets (currencies, metals) → price stability

- Transformation → Alters money flows, cross-border payments, trade finance

- Binary choice → Adapt (↑integration) vs resist (risk exclusion)

- Global impact → No nation insulated from systemic change

India’s Position & Policy Tensions

- Current status → No legalisation; transactions taxed (30% + 1% TDS)

- RBI stance → Push for ban on private cryptos; CBDC pilots underway

- CBDC vs Stablecoins → CBDC = legal backing; stablecoins = private innovation

- Policy dilemma → Harness innovation ✦ contain risks (fraud, volatility, illicit flows)

Strategic & Economic Context

- India’s leverage → Strong shock absorption, evolving global economic weight

- Global shifts → Wars, rivalries → new coalitions, fractured alliances

- Strategic independence → Needs agility, vigilance, performance (no complacency)

- Role in G20 → India advocating global crypto regulations & coordinated approach

Key Implications

- Financial stability → Stablecoins may bypass banks, affect monetary policy

- Sovereignty risk → Private currency vs state-issued legal tender

- Tech opportunity → Blockchain, cross-border remittance, fintech growth

- Regulatory urgency → Balance innovation ↔ stability; global harmonisation essential